Higher Bund yields: The relative resilience of Emerging Market sovereigns

21.05.2021Company: Amcham

Emerging Market sovereign bonds have shrugged off the troubles of their eurozone peers. But rising Bund yields weigh on appetite for longer maturity bonds while rich relative valuations could pressure spreads in the near term. That said, the longer-term outlook remains favourable

In this article

EM sovereign spreads shrug off eurozone troubles

Rising core rates have weighed on total returns for Emerging Market sovereign hard currency bonds this year. Here, EM EUR sovereign bonds (-1.8% YTD total return based on Bloomberg Barclays EM Pan Euro Aggregate: Sovereign Index) have fared somewhat better than their USD peers (-2.8% for Bloomberg Barclays EM Sovereign Index Unhedged EUR) due to the more modest rise in German Bund yields vs US Treasuries and a shorter duration of the EM EUR sovereign space (modified duration of 7.9yrs vs 8.8yrs for the respective indices).

However, appetite for EM debt remains strong, with the Institute of International Finance (IIF) reporting US$87bn of portfolio flows between January and April this year. This has supported EM EUR sovereign credit spreads which have largely shrugged off the recent rise in Bund yields and the sell-off in eurozone government bonds (EGBs) with the EM Pan Euro Aggregate: Sovereign Index spread having narrowed by 7bp year-to-date.

Importantly, two key drivers behind the recent EGB sell-off have played less of a role for EM, notably the uncertainty about PEPP which should only weigh on eligible eurozone bonds and secondly, primary market supply which picked up in April but is not exceptionally high, as you can see in the chart below.

EM EUR debt issuance (€bn)

![Source: Bond Radar, ING – CEE includes Albania, Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Montenegro, North Macedonia, Poland, Romania, Serbia, Slovakia, Slovenia]()

Source: Bond Radar, ING – CEE includes Albania, Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Montenegro, North Macedonia, Poland, Romania, Serbia, Slovakia, Slovenia

Bund curve steepening and relative valuations warrant caution but long-term outlook is favourable

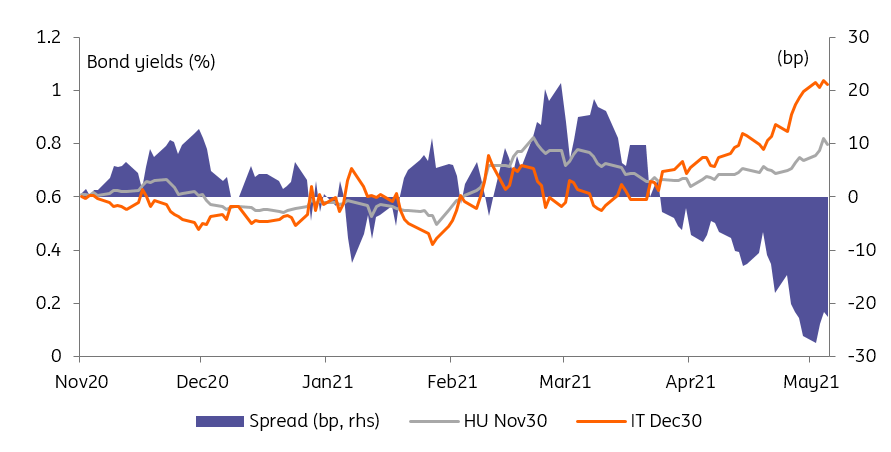

That said, in client conversations, we note there is a lack of appetite for longer maturity bonds due to the curve steepening pressure in Bunds. Moreover, some EM EUR, particularly CEE bonds, screen rich in a historical relative value context against EGBs owing to the latter's underperformance, with Croatian euro-denominated sovereign bonds (CROATI) currently trading at flattish yields to Italian BTPS (vs 30/35bp wider in mid-March) and Hungarian bonds (REPHUN) trading 20-25bp inside BTPS (compared to 0bp on average over the last six months).

REPHUN bonds also trade close to all-time tights vs Portuguese PGBs (REPHUN 0.5% 30 trade 25bp wider vs PGB 0.475% 30 vs 50bp 6-month average). All in all, this could put some pressure on EM EUR spreads in the near term. With liquidity proving more challenging in EM EUR, we also see the risk of price discoveries leading to gaps in pricing.

BTPS 1.65% 30 vs REPHUN 0.5% 30

![Refinitiv, ING]()

Source:Refinitiv, ING

However, based on our rates strategist view that the sell-off should be front-loaded and contained (the ING view is for the 10yr Bund at 0.20% in the fourth quarter of 2021), we believe that demand for carry in EM EUR is here to stay and therefore we only expect a limited spread widening.

We also consider the fundamentals of CEE issuers, the dominant region in EM EUR, as favourable, further supported by the NextGen EU recovery fund prospects. Indeed they are serial upgrade candidates; S&P and Fitch upgraded Hungary to BBB in 2019 and Moody's Baa3 rating has a positive outlook, Croatia gained investment-grade status in 2019, and Fitch placed Bulgaria's BBB rating on a positive outlook in February.

Net primary supply (issuance minus redemptions) by CEE issuers should be limited; we expect c.€11bn equivalent in 2021 vs €21bn in 2020.

Authors

Trieu Pham

Emerging Markets Sovereign Debt Strategist

Antoine Bouvet

Senior Rates Strategist

This article is part of

Higher Bund yields: The complete picture

Tags: Law | Economics |